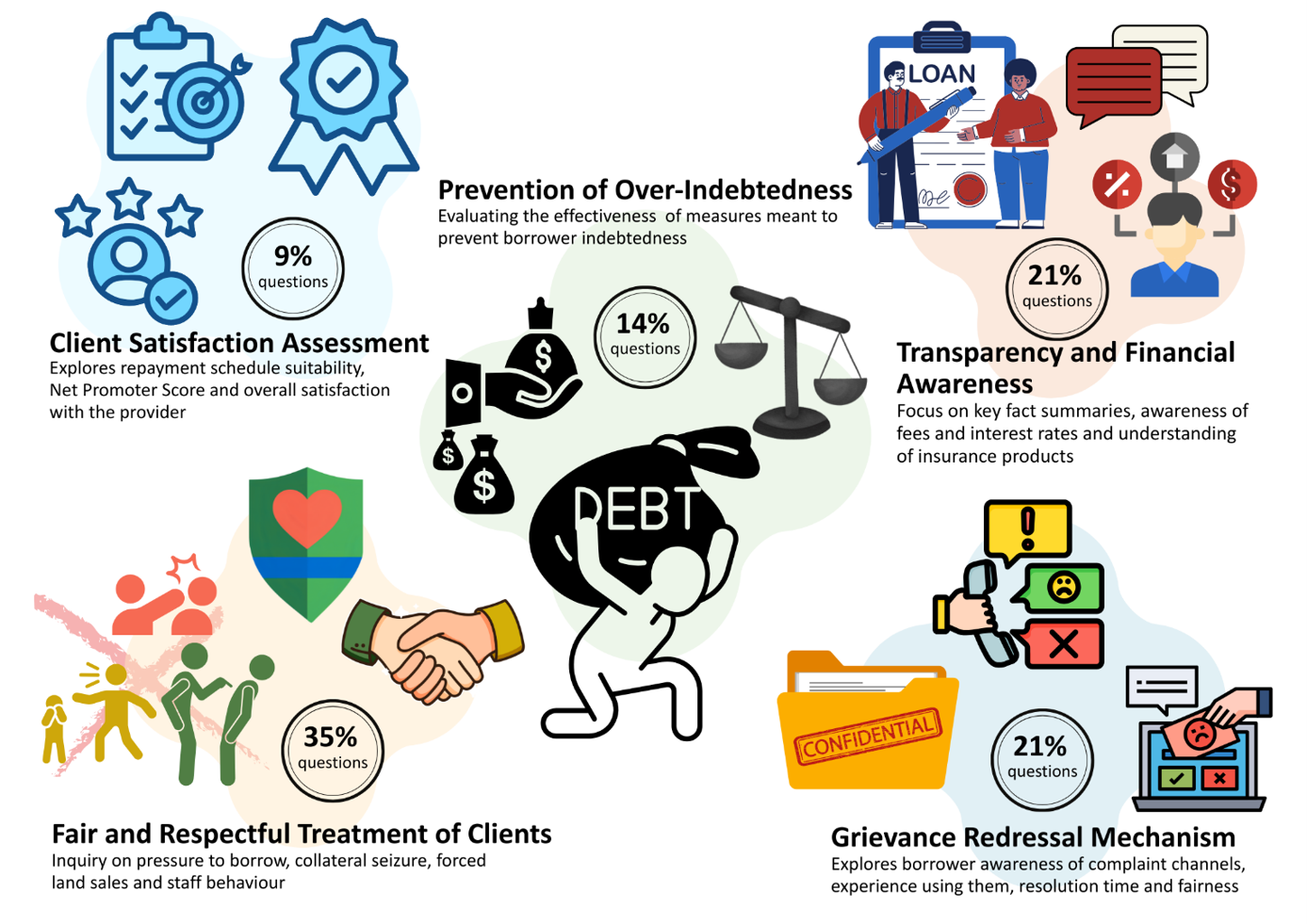

Cambodia's financial sector is at an inflection point — and client voices are showing us where the gaps are.

As part of the Harmonized Code of Conduct Assessments mandated by The Association of Banks in Cambodia (ABC), Cambodia Microfinance Association (CMA), and the National Bank of Cambodia (NBC), M-CRIL assessed 15 FSPs and interviewed 585 borrowers across 9 provinces to understand how responsible finance practices are experienced on the ground.

Our findings point to five priority areas: over-indebtedness, transparency and financial awareness, fair treatment of clients, grievance redressal, and client satisfaction.

This is the first in a series of advisory notes that will unpack each theme with evidence and recommendations.

Watch this space.

Read Advisory Note 1: M-CRIL's Microscopic View of Responsible Financing Practices in Cambodia

M-CRIL presents its latest knowledge product, as of end-July 2025. This document presents a unique, updated mega-analysis of the contemporary microenterprise sector in India. It is the second publication in a series focused on microenterprises in India. The first publication, "Microenterprise Mela: Size & Diversity of the Microenterprise Sector in India," was released in September 2024. This microenterprise research has been undertaken by M-CRIL as a contribution to the understanding of the sector for the design and support of enterprise promotion programmes. Further documents in this series will be released in due course.

Microenterprise Mela-2: Variations in employment & productivity in India’s diverse microenterprises is a mega-analysis based on the latest data on the microenterprise sector released in January 2025 by the National Sample Survey Office (NSSO) of the Ministry of Statistics and Programme Implementation (MoSPI) of the Government of India. As for our first Microenterprise Mela publication using data for 2022-23, this document combines data from the Annual Survey of Unincorporated Sector Enterprises (ASUSE) with M-CRIL’s 40+ years of experience studying every aspect of microenterprises in India and in more than a dozen other countries in Asia, as well as parts of Africa and diverse other countries (total ~35). During this time, we have undertaken hundreds of field studies, desk research and analysis of data from microenterprise and microfinance surveys conducted by us and also by other institutions (including the NSSO).

We welcome comments, reflections and discussion of the analysis and findings presented in this document.

M-CRIL is pleased to share its latest knowledge product: a meta-analysis based on the latest data on the microenterprise sector released in July 2024 by the National Sample Survey Office (NSSO) of the Ministry of Statistics and Programme Implementation (MoSPI) of the Government of India. This document combines data from the above Annual Survey of Unincorporated Sector Enterprises (ASUSE) with M-CRIL’s 40+ years of experience studying every aspect of microenterprises in India and in a dozen other countries in Asia as well as to some extent in Kenya, Uganda, Ethiopia, Ghana, South Africa and diverse other countries (total ~35). During this time, we have undertaken hundreds of field studies, desk research and analysis of data from microenterprise and microfinance surveys conducted by us and also by other institutions (including the NSSO).

We believe the attached document is a Unique meta-analysis of the contemporary microenterprise sector in India. It has been undertaken by M-CRIL as a contribution to the understanding of the sector for the design and support of enterprise promotion programmes.

We welcome comments, reflections and discussion of the analysis and findings presented in this initial document.

In 2023, M-CRIL was commissioned to undertake a Thematic Global Evaluation of the UN Joint SDG Fund’s country-level SDG financing portfolio

The evaluation report is now public and is available at https://jointsdgfund.org/publication/thematic-global-evaluation-joint-sdg-funds-sdg-financing-enabling-environmental – attached here for quick access to the main report.

This evaluation explored the performance of 61 country-level JPs that form the SDG Financing: Enabling Environment Portfolio for the period June 2020 to June 2023. The overall evaluation approach was to document direct programme results, emerging impact and broader systemic changes to strengthen the mobilization or improve utilization of financial resources to meet the demonstrated needs of SDG promotion in a broad range of countries.

As part of this evaluation, 7 country case studies spread across the five United Nations Development Coordination Office (UNDCO) regions were conducted – Mongolia, Nepal (Asia Pacific), Kyrgyzstan (ECA), Jordan (MENA) Guinea (Conakry), Comoros (SSA) and Costa Rica (LAC). The choice of case study countries was based on both regional and effectiveness considerations. The aim was to cover JPs that were at diverse levels of progress and maturity.

For this evaluation, the M-CRIL Evaluation Team analysed a large database of annual progress and final reports from the country-level JPs plus other information provided by the Joint SDG Fund. The evaluation found an extensive and growing commitment from country governments to finding resources for the funding of SDGs. Key constraints included lack of experience with targeted budgeting of the sort needed for the funding approach advocated by the Joint SDG Fund as well as limited domestic as well as international resources. In this context, the evaluation documents a range of innovative financing measures devised in a variety of countries. The report makes exciting reading in this context.

Download the main report

In late 2022, Cambodia Microfinance Association (CMA) commissioned M-CRIL Limited to conduct an independent impact assessment of the microfinance sector in Cambodia. This study, the first of its kind in the country, draws on survey responses from over 3,200 #microfinance client households and 40+ qualitative interactions across 10 provinces and more than 450 villages in the country. The survey was undertaken in January-February 2023 and analysis, report writing and revisions took place mainly up to August 2023.

CMA hosted an in person and virtual conference for stakeholders on 19 January 2024 at the Center for Banking Studies (CBS), Phnom Penh to disseminate the results.

Sanjay Sinha, Co-Founder & Managing Director, M-CRIL and team leader for this impact assessment study presented the key findings during the event with remote support from India by Ratika Kathuria, AVP, Research and Evaluation, who was the Research Manager for the study. We gratefully acknowledge the support of the field team of enumerators and supervisors, M-CRIL’s team in Cambodia (Sengdy Khiev and Country Manager, Shayandeep Chakraborty), data management support by Analysts in India (Arpana Gone, Shwetangi Raj and Rejoice Parackal) as well as ongoing inputs and advice on methodology from M-CRIL’s co-Founder and Director Frances Sinha.

M-CRIL thanks CMA – Chairman Sok Voeun, Secretary General Phal Vandy, and Head of Financial Inclusion and Social Impact Pheakyny Vong – for commissioning the study and the CMA Board for their comments on various versions of the report.

The report is now public and available at https://cma-network.org/km/information-center/cma-publication/

We hope and expect that the report will make an evidence-based contribution to the controversies around the performance and approach of Cambodian MFIs towards lending to low-income families and create a better understanding of the nuanced impact of microfinance on micro-borrower households in the country.

Here are some glimpses of the event.

"Catching up with Climate Change: A brief exploration of the Green Finance Landscape" by Charlene Miriam Samuel for M-CRIL reveals that global green finance efforts fall far short of climate goals. Public finance dominates adaptation funding worldwide, with limited private sector data. India faces a similar gap. India requires a well-defined strategy that includes the government, the Reserve Bank of India and the financial sector to support green finance. To tackle climate change, robust policy frameworks, blended finance and non-financial incentives are needed. The climate financing framework worldwide needs to be substantially enhanced to achieve a sustainable world

Read more

The Glossary of Key Financial Inclusion Terms that M-CRIL prepared for Alliance for Financial Inclusion (AFI) by an M-CRIL team led by Mr Sanjay Sinha, our Co-Founder & Director is now in digital print, ‘Words Matter – AFI’s Financial Inclusion Dictionary’. Other M-CRIL members who supported the preparation of the definitions were Ujjwal Dadhich, Arpita Pal Agrawal and Tirupathaiah Namani.

This special report is a product of AFI’s Gender Inclusive Finance workstream and serves as a guide for AFI staff, members, and stakeholders to understand how AFI interprets and employs various terms and concepts.

It does not purport to provide definitive global definitions but rather, it aims to serve as an intersectional resource to promote an inclusive and appropriate language to assist in the formulation of policies and regulations.

Read more

M-CRIL is extremely pleased to be part of this Ethnographic Study to Explore the Impacts of Micro and Small Enterprise (MSE) Finance in India to understand their pathways to entrepreneurship, digitization journeys, covid impacts, financial and non-financial needs. This study was supported by CGAP.

CGAP's latest focus note advocates the importance of taking a segmented approach to addressing MSE needs. It draws on primary research with 383 MSEs in India, Kenya, and Peru to show that a more tailored and differentiated set of financial services for MSEs based on their different needs is critical to ensuring their growth and inclusion. It recommends segmenting along 5 specific dimensions:

Segmenting the MSE market using these dimensions can help FSPs to better serve their clients. It can also help the broader financial inclusion sector as it seeks to rebuild the MSE ecosystem in an inclusive and resilient manner in the wake of the ongoing COVID- 19 pandemic.

Please follow the link to read the exec summary or full report,

Download the Executive Summary

Download the Full Publication

How is climate change impacting the poor and how financial institutions can contribute to creating a coping environment. A short presentation for an FWWB dialogue on Managing Climate Risk.

Read more

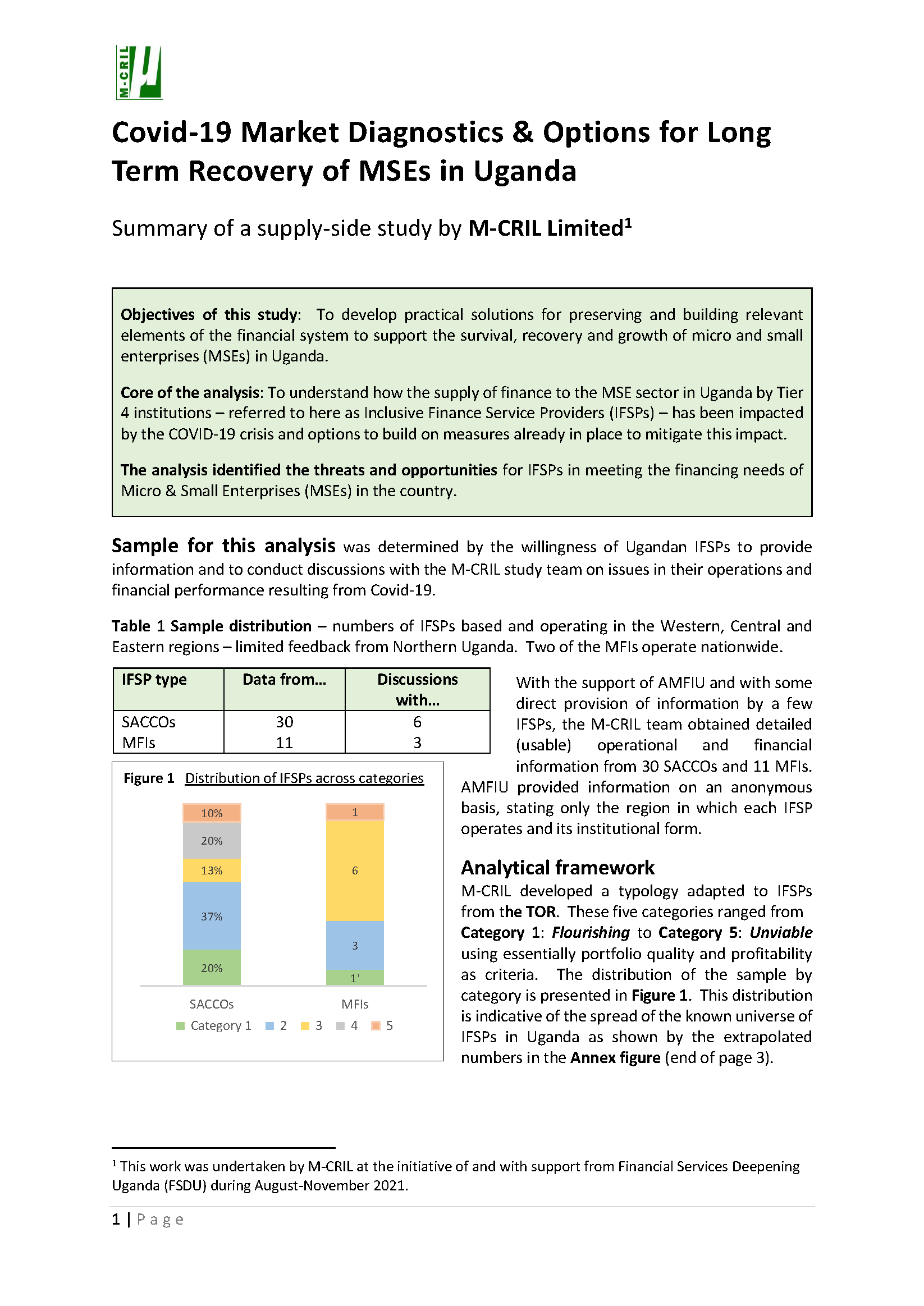

Herewith, the current M-CRIL analytics on the effects of Covid-19 on the performance of inclusive finance service providers (IFSPs) in Uganda emerging from our recent analytics of IFSPs – the Uganda microfinance sector – to develop practical solutions for preserving and building relevant elements of the financial system to support the survival, recovery and growth of micro and small enterprises (MSEs) in the country. This work was undertaken by M-CRIL at the initiative of and with support from Financial Services Deepening Uganda (FSDU) during August-November 2021.

Read more

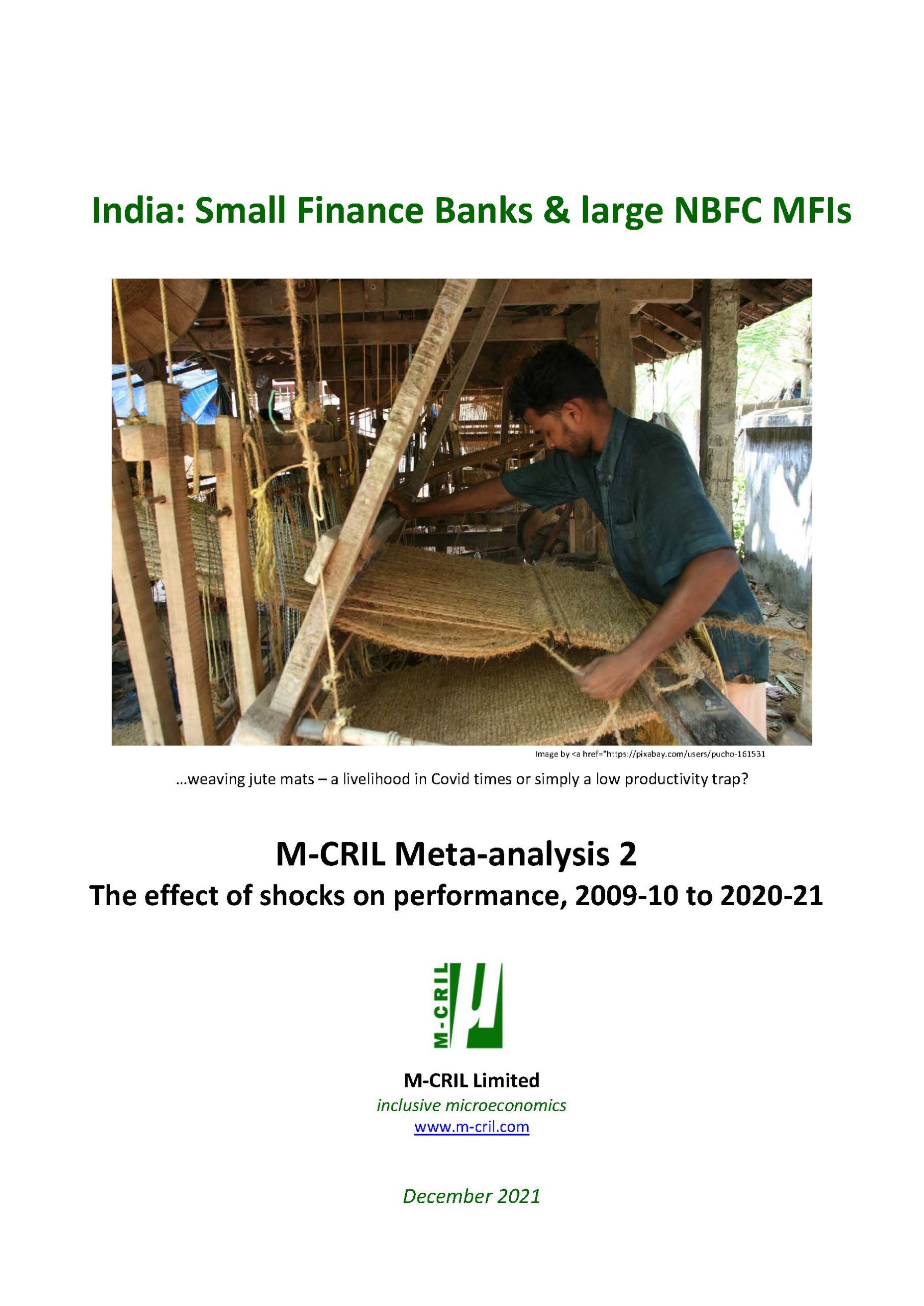

Microlenders in India - Small Finance Banks and NBFC-MFIs have had to contend with repeated shocks, from both policy and nature, over the past 12 years - 2009-10 to 2020-21. This infographic shows the effect of these shocks on the financial performance of these institutions; the pattern is repetitive.

This document follows from the previous M-CRIL infographic – Meta-analysis 1: Size, Growth & Performance 2020-21 published on November 2021

Read more

A brief infographic on the growth and performance of India's inclusive finance service providers (Small Finance Banks and large NBFC MFIs) in the shadow of the pandemic - the story to end-March 2021. Fingers crossed for the immediate future.

Read more

This is an infographic on the MFI sector in Nepal and its performance over the past couple of years. It presents some key indicators of market share, growth and performance for Nepali financial year 2076-77 (July 2019-July 2020); the document covers 20 of the largest MFIs in Nepal. A key finding is that there is a stark difference in the performance of Nepali MFIs over the past two years.

Read more

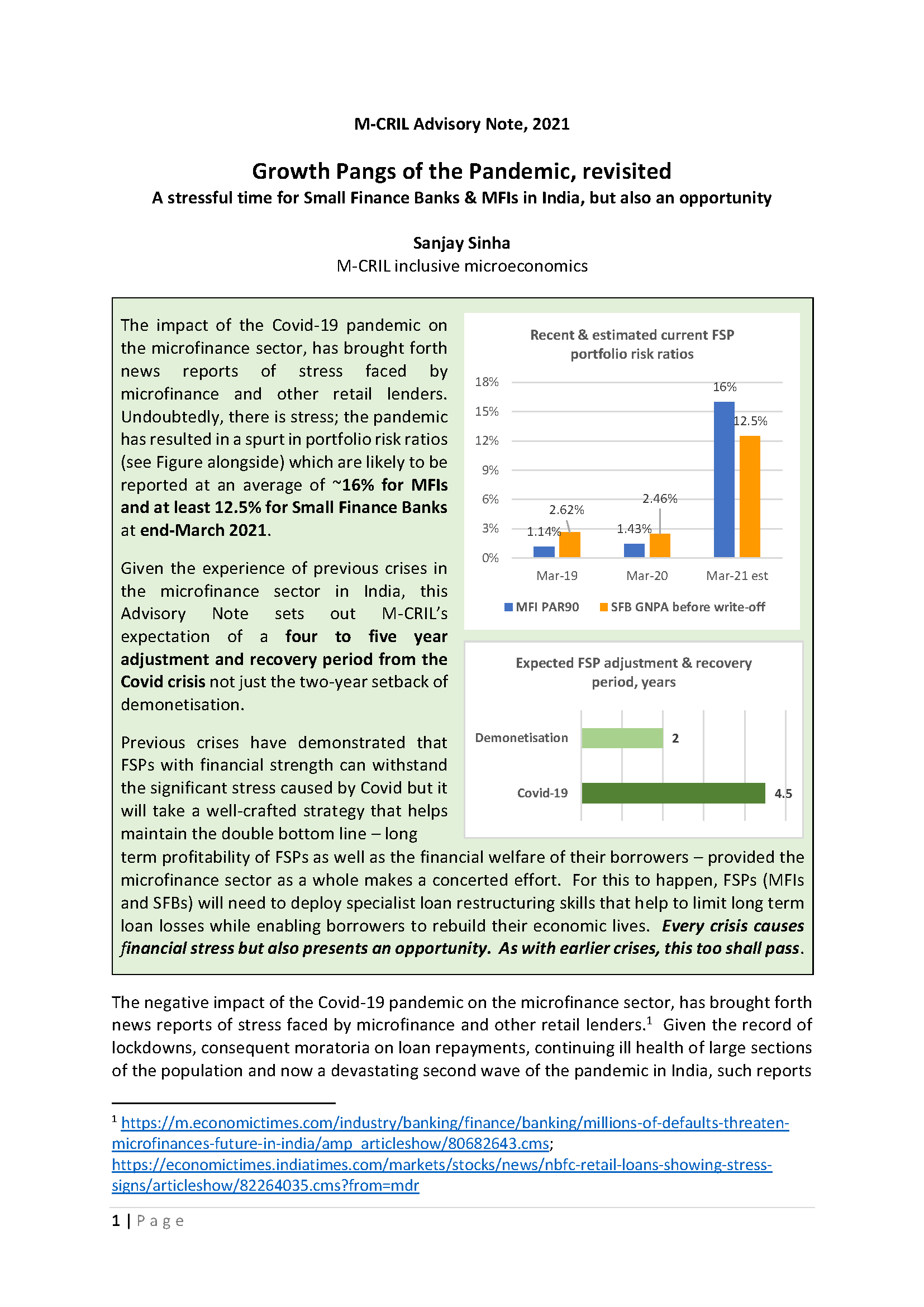

The impact of the Covid-19 pandemic on the microfinance sector, has brought forth news reports of stress faced by microfinance and other retail lenders. Given the experience of previous crises in the microfinance sector in India, this Advisory Note sets out M-CRIL’s expectation of a four to five year adjustment and recovery period from the Covid crisis not just the two-year setback of demonetisation.

Previous crises have demonstrated that FSPs with financial strength can withstand the significant stress caused by Covid but it will take a well-crafted strategy that helps maintain the double bottom line – long term profitability of FSPs as well as the financial welfare of their borrowers – provided the microfinance sector as a whole makes a concerted effort. For this to happen, FSPs (MFIs and SFBs) will need to deploy specialist loan restructuring skills that help to limit long term loan losses while enabling borrowers to rebuild their economic lives. Every crisis causes financial stress but also presents an opportunity. As with earlier crises, this too shall pass.

Read more

This synthesis document brings together selected aspects of the Covid-19 Microfinance Liquidity Tour of Asia undertaken by M-CRIL over the past few months. In this document, we have compiled cross country data emerging from the M-CRIL Advisory Notes covering different types of MFSPs and provided some reflections on the analysis.

Read more

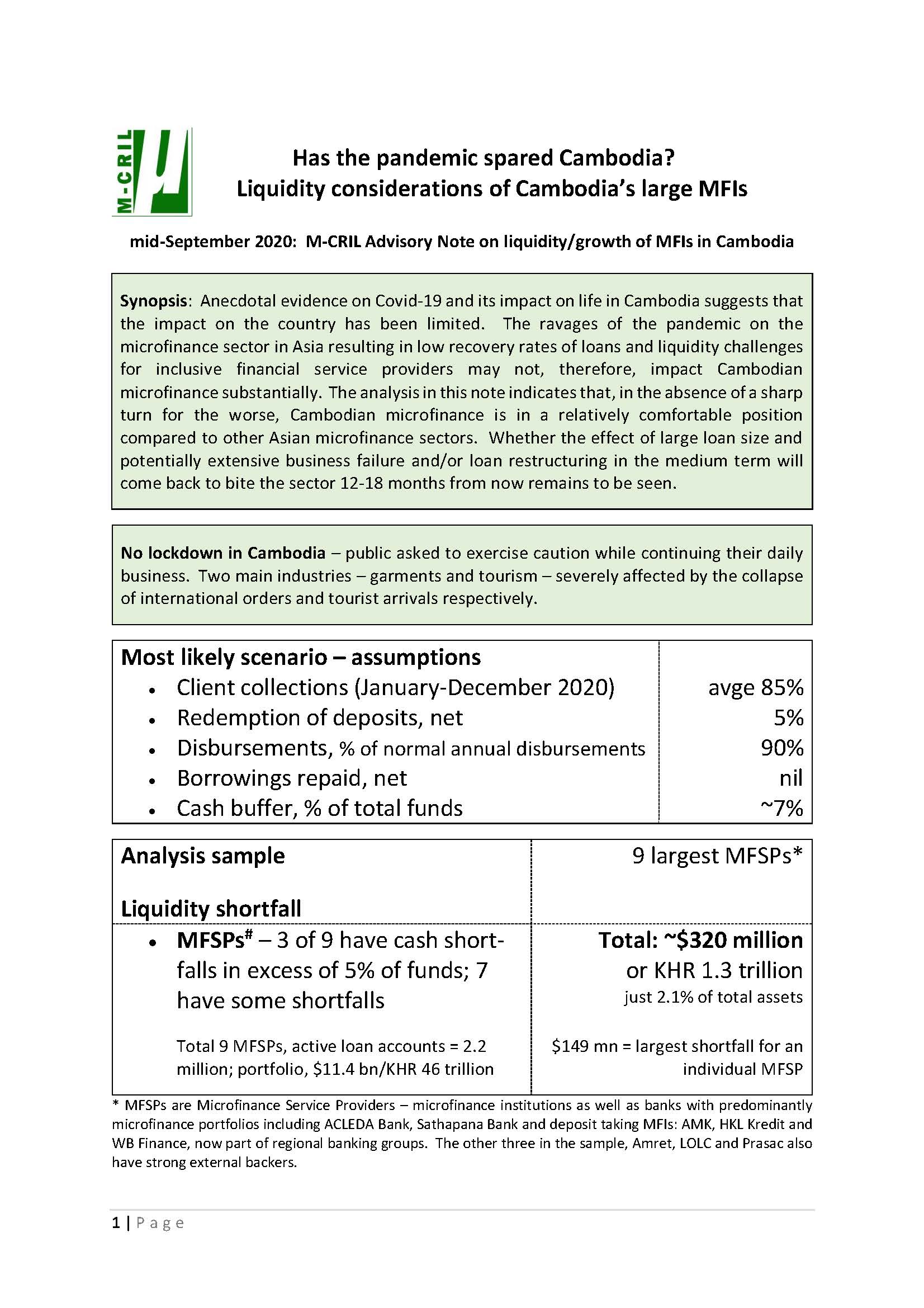

Anecdotal evidence on Covid-19 and its impact on life in Cambodia suggests that the impact on the country has been limited. The ravages of the pandemic on the microfinance sector in Asia resulting in low recovery rates of loans and liquidity challenges for inclusive financial service providers may not, therefore, impact Cambodian microfinance substantially. The analysis in this note indicates that, in the absence of a sharp turn for the worse, Cambodian microfinance is in a relatively comfortable position compared to other Asian microfinance sectors. Whether the effect of large loan size and potentially extensive business failure and/or loan restructuring in the medium term will come back to bite the sector 12-18 months from now remains to be seen.

Read more

The client protection principles and their indicators have been developed for ‘normal’ times. There is no specific guidance on protecting clients when a pandemic puts every household at risk and market closure means that clients cannot earn: when ‘over-indebtedness’ has become complete inability to pay the instalments on outstanding loans due to factors outside the control of the client or the lending institution.

Looking at the situation particularly in India, and for a small urban MFI that Frances Sinha is associated with, she reflects on the responsible measures that are needed in these challenging times through this article published by The Boulder Institute of Microfinance

Read more

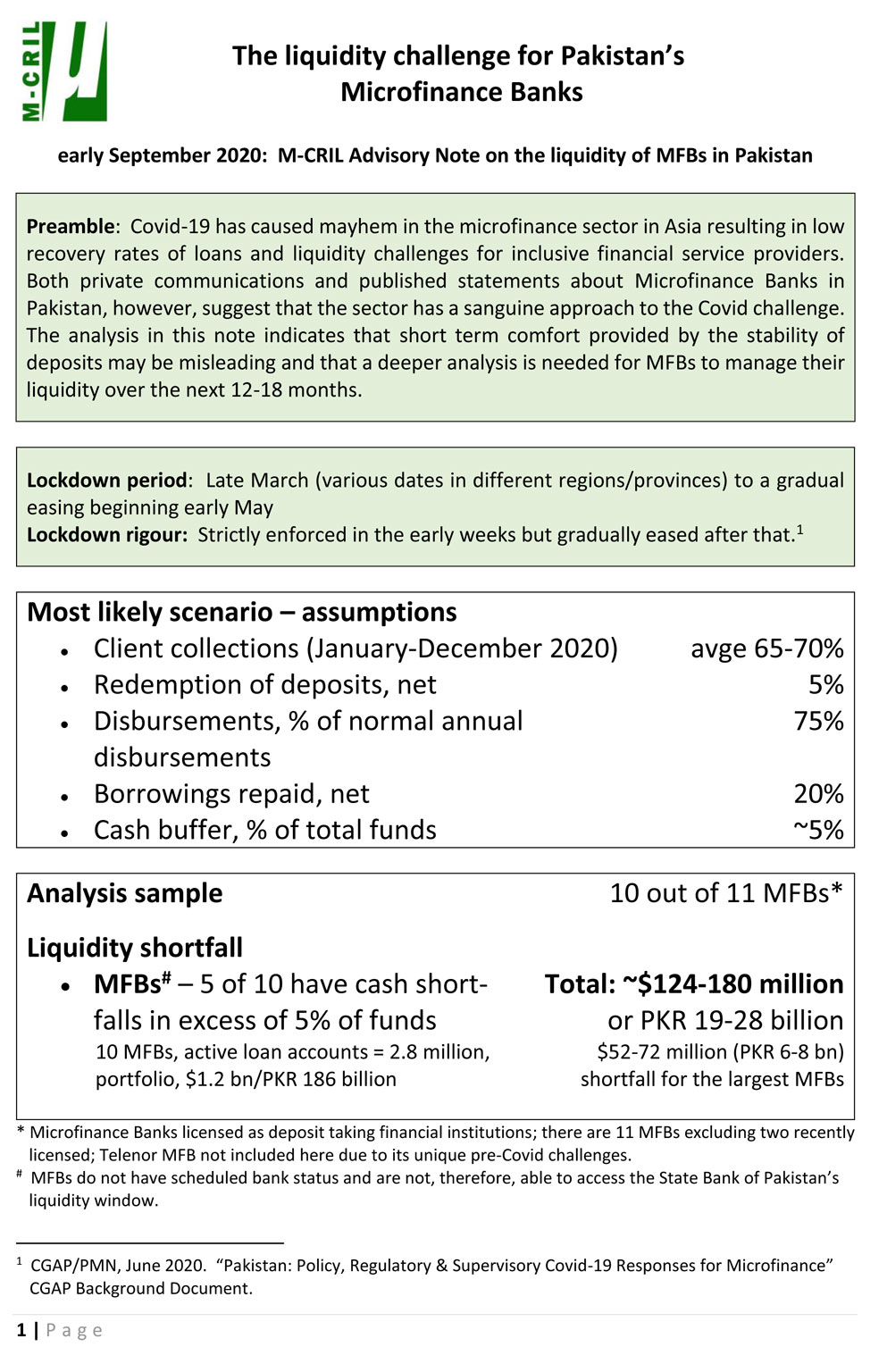

Covid-19 has caused mayhem in the microfinance sector in Asia resulting in low recovery rates of loans and liquidity challenges for inclusive financial service providers. Both private communications and published statements about Microfinance Banks in Pakistan, however, suggest that the sector has a sanguine approach to the Covid challenge. The analysis in this note indicates that short term comfort provided by the stability of deposits may be misleading and that a deeper analysis is needed for MFBs to manage their liquidity over the next 12-18 months.

Read more

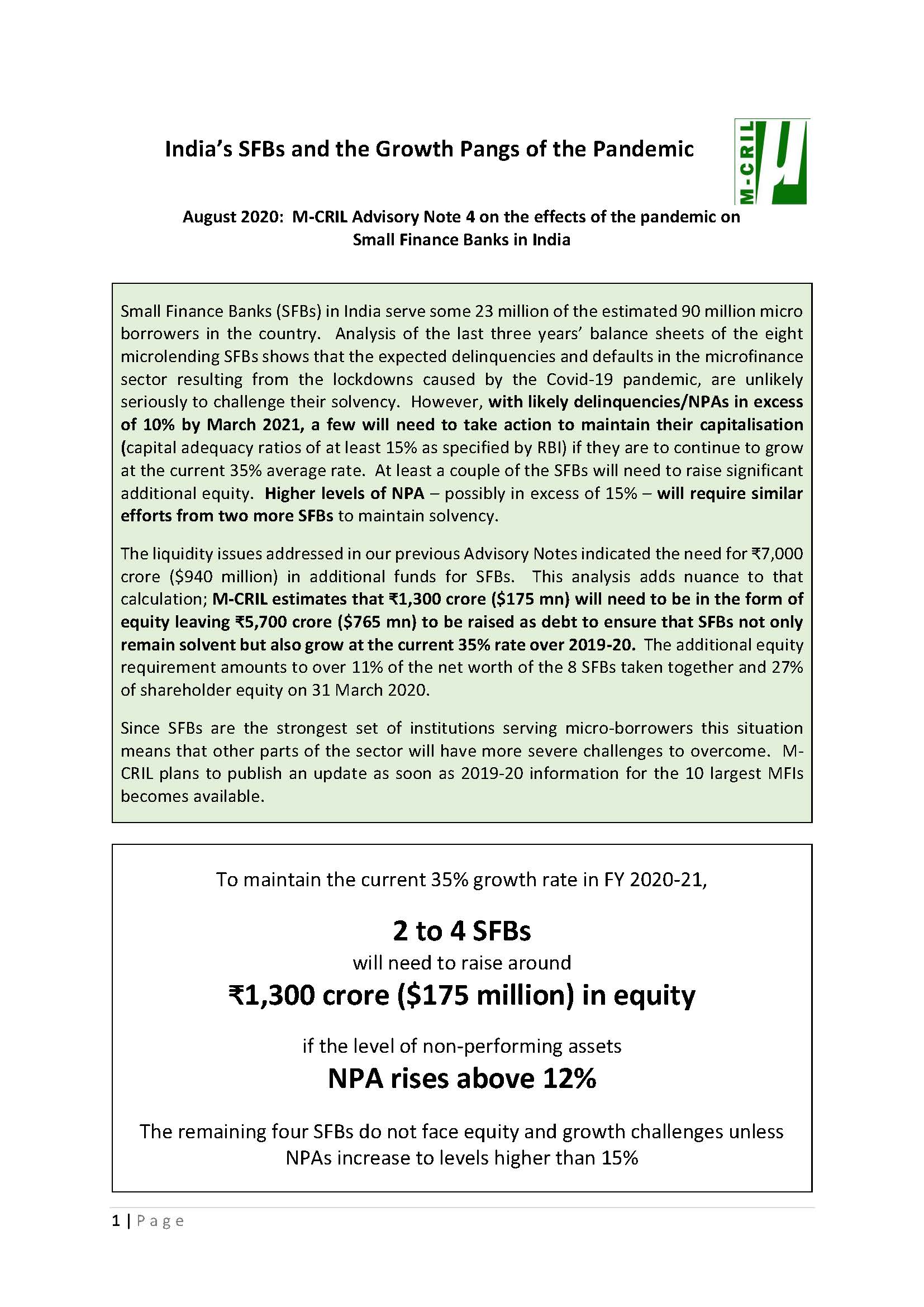

Analysis of the last three years’ balance sheets of the eight microlending SFBs shows that the expected delinquencies and defaults in the microfinance sector resulting from the lockdowns caused by the Covid-19 pandemic, are unlikely seriously to challenge their solvency. However, with likely delinquencies/NPAs in excess of 10% by March 2021, a few will need to take action to maintain their capitalisation. Our previous Advisory Notes indicated the need for ₹7,000 crore ($940 million) in additional funds for SFBs. This analysis adds nuance to that calculation; M-CRIL estimates that ₹1,300 crore ($175 mn) will need to be in the form of equity leaving ₹5,700 crore ($765 mn) to be raised as debt to ensure that SFBs not only remain solvent but also grow at the current 35% rate over 2019-20. The additional equity requirement amounts to over 11% of the net worth of the 8 SFBs taken together and 27% of shareholder equity on 31 March 2020. Since SFBs are the strongest set of institutions serving micro-borrowers this situation means that other parts of the sector will have more severe challenges to overcome.

M-CRIL plans to publish an update as soon as 2019-20 information for the 10 largest MFIs becomes available.

Read more

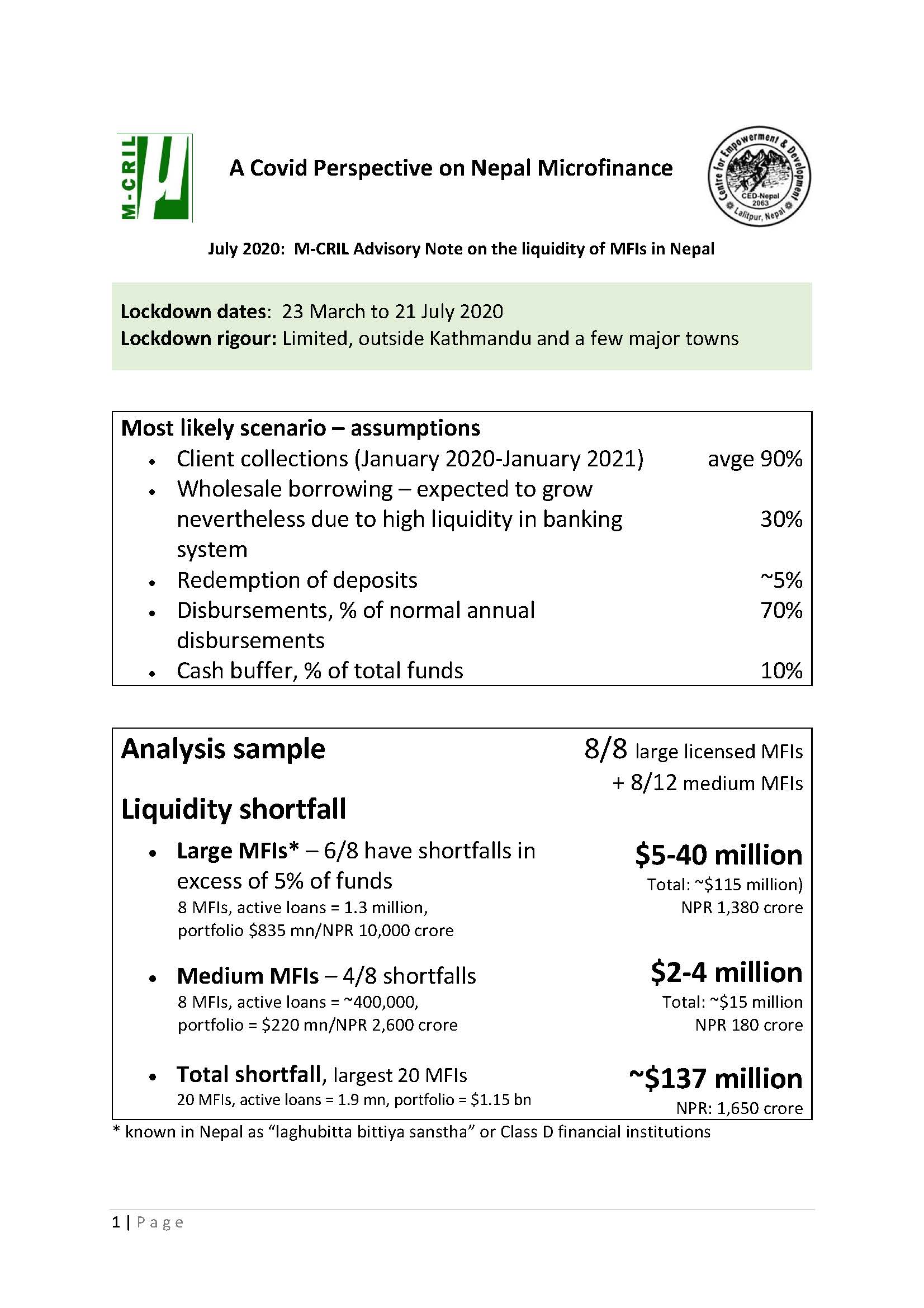

This analysis of the microfinance scenario in Nepal is the third in the series of M-CRIL Advisory Notes on liquidity in microfinance sectors in Asia. It follows our detailed analysis of liquidity in Indian and Myanmar microfinance. It shows a less troubled situation than in India but points to potential issues resulting from the microfinance demand of Nepali migrant workers returning from other countries.

Read more

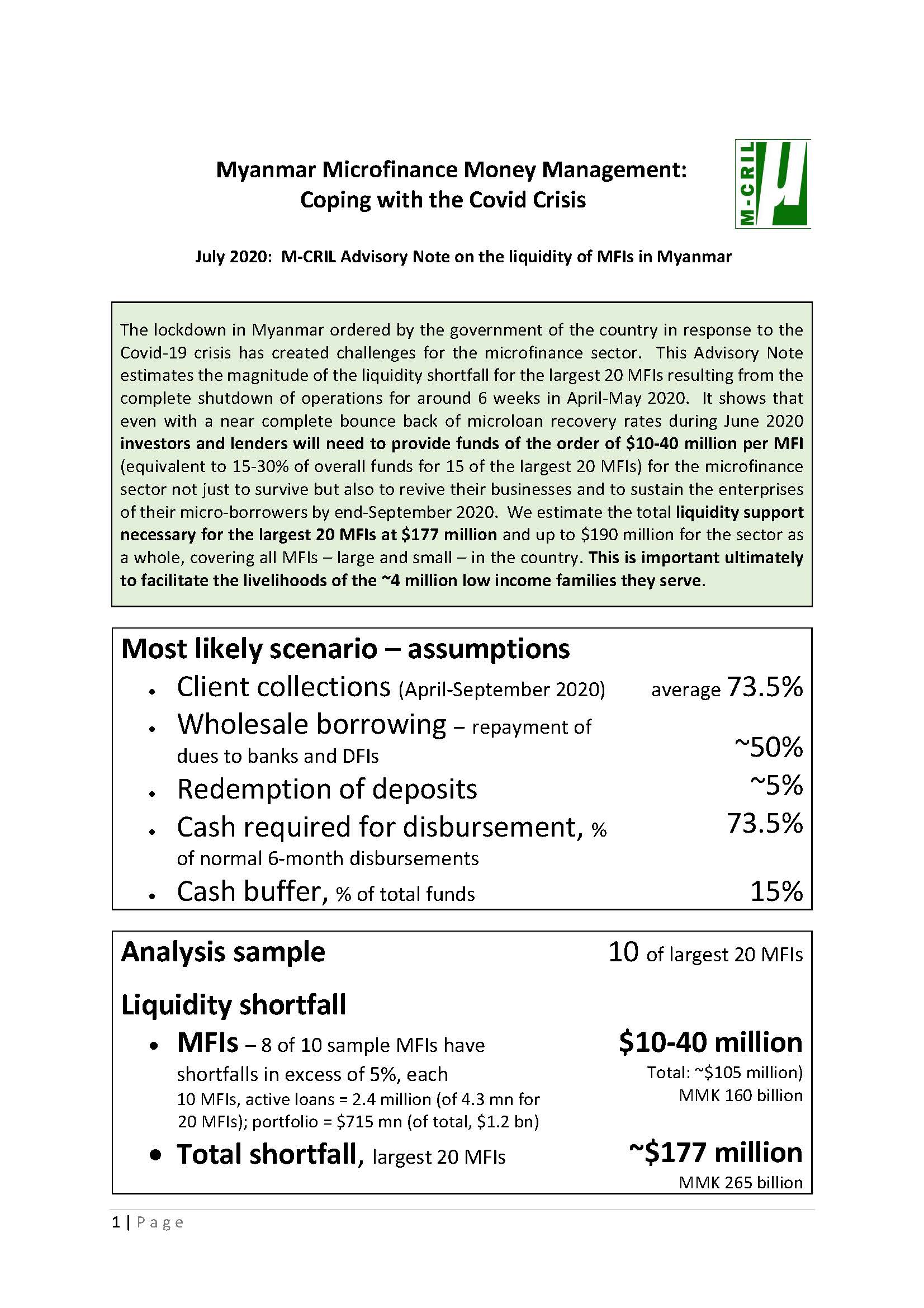

The lockdown in Myanmar ordered by the government of the country in response to the Covid-19 crisis has created challenges for the microfinance sector. This Advisory Note estimates the magnitude of the liquidity shortfall for the largest 20 MFIs resulting from the complete shutdown of operations for around 6 weeks in April-May 2020. It shows that even with a near complete bounce back of microloan recovery rates during June 2020 investors and lenders will need to provide funds of the order of $10-40 million per MFI (equivalent to 15-30% of overall funds for 15 of the largest 20 MFIs) for the microfinance sector not just to survive but also to revive their businesses and to sustain the enterprises of their micro-borrowers by end-September 2020. We estimate the total liquidity support necessary for the largest 20 MFIs at $177 million and up to $190 million for the sector as a whole, covering all MFIs – large and small – in the country. This is important ultimately to facilitate the livelihoods of the ~4 million low income families they serve.

Read more

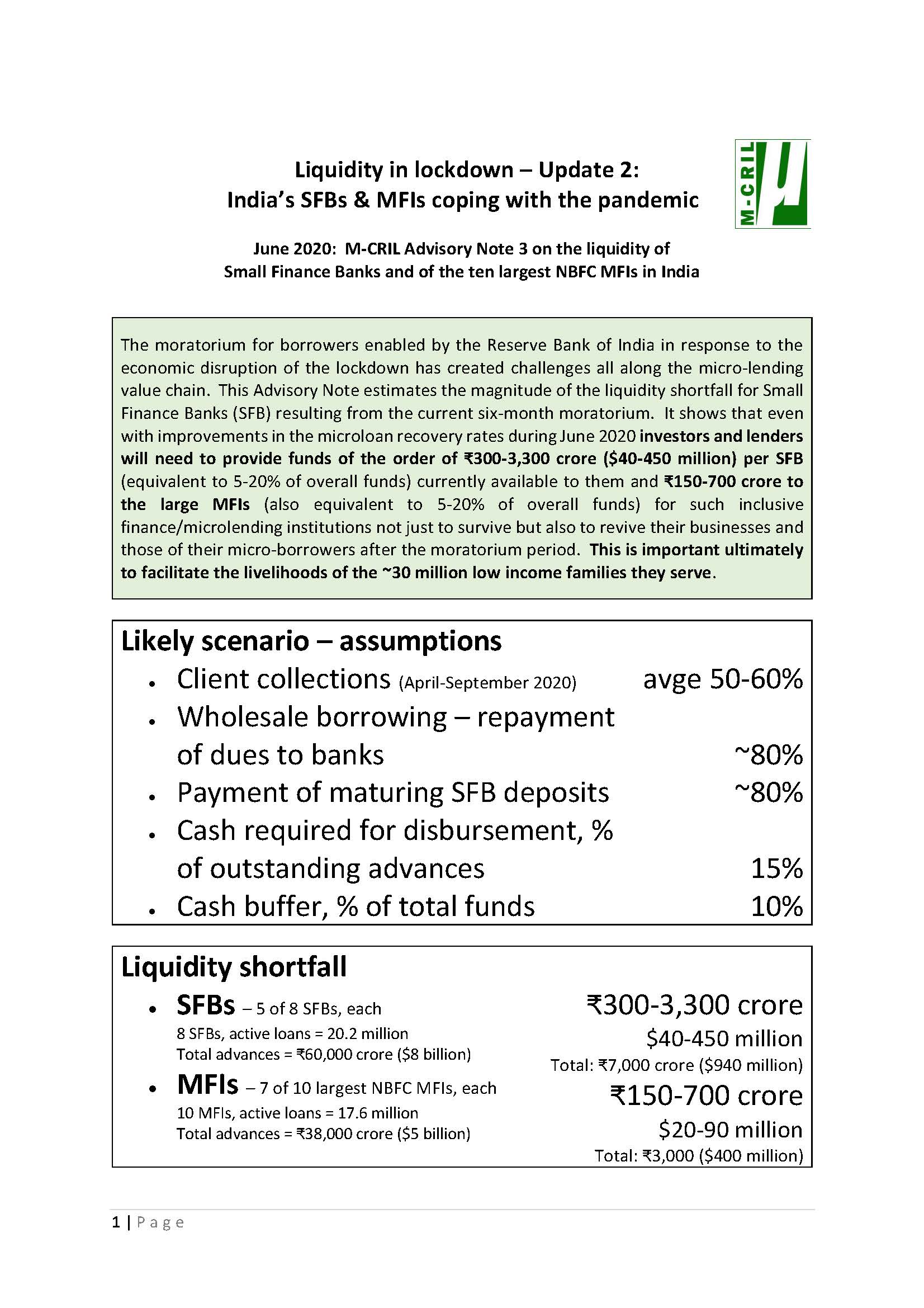

[Version 3 covering MFIs as well as SFBs] The moratorium for borrowers enabled by the Reserve Bank of India in response to the economic disruption of the lockdown has created challenges all along the micro-lending value chain. This Advisory Note estimates the magnitude of the liquidity shortfall for Small Finance Banks (SFB) resulting from the current six-month moratorium. It shows that even with improvements in the microloan recovery rates during June 2020 investors and lenders will need to provide funds of the order of ₹300-3,300 crore ($40-450 million) per SFB equivalent to 5-20% of the overall funds available to the SFBs not just to survive but also to revive their businesses after the moratorium period. Similarly, for MFIs there are liquidity shortfalls of ₹150-700 crore ($20-90 million). This is important ultimately to facilitate the livelihoods of the low income families they serve. Bankers who provide wholesale loans to SFBs and MFIs need to shed their conservatism and step up with a dynamic response to the current situation.

Read more

India has now surpassed Britain, its former colonial master, as the world's fifth largest economy. In spite of Covid it continues to be regarded by the IMF as the world's fastest growing large economy. Why then does the government act like its policy options are limited in its response to the economic crisis resulting from the pandemic?

- Sanjay Sinha, Managing Director, M-CRIL inclusive microeconomics, Financial inclusion and microenterprise specialist, former UN Advisor on Inclusive Finance

Every crisis presents an opportunity. The reverse migration of large numbers of semi-skilled and unskilled labour is an apparently unfortunate fallout of the current lockdown. The Government has been miserly in its response to the miseries of migrants. Yet the additional allocation to MNREGA and various other pots of money could contribute to a stimulation of the agricultural economy of eastern India.

The purpose of this article is to suggest that this reverse migration does not need to become an unmitigated disaster; indeed, it can be turned into an opportunity for the successful transformation of the countryside in the least developed parts of the country.

- Sanjay Sinha, Managing Director, M-CRIL inclusive microeconomics, Financial inclusion and microenterprise specialist, former UN Advisor on Inclusive Finance

Microfinance Alert in Cambodia: Real Issues or Scaremongering?

M-CRIL has undertaken an analysis of the recent damning report by LICADHO Cambodia on the conduct of Cambodian MFIs towards their borrowers titled, COLLATERAL DAMAGE: Land loss and abuses in Cambodia’s microfinance sector

Read M-CRIL’s Advisory Notes on the LICADHO Report

Note 1: The evidence for the allegations made and the likely scale of the problem

Note 3: Microfinance Alert in Cambodia: How significant is individual lending?.

There is a push for digitizing payments across the board in India. This has picked up steam after the demonetization of large currency notes in November 2016. But how ready and willing are low-income Indians (as well as low-income people in other developing countries) to adopt digital payments? This question needs more thought as there is a range of issues around mobile phone penetration, bank account features, acceptance of digital payments across value chains, and the viability of small transactions.

Keywords: financial inclusion, fintech, digital literacy

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

Guidelines on Outcomes Management for Financial Service Providers, Social Performance Task Force

READ MORE

MIS as a potential catalyst for social performance management

READ MORE

Social Rating and Social Performance Reporting in Microfinance

READ MORE

End to end approach to effective data for SPM

READ MORE

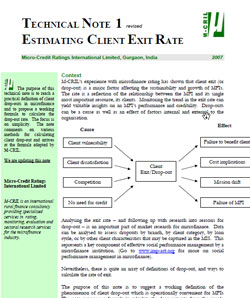

Estimating Client Exit Rate

READ MORE

Estimating Sample Size

READ MORE

Can MFIs Achieve the Double Bottom Line?

READ MORE

Smart regulation for inclusion

READ MORE

Of interest rates, margin caps & poverty lending – How the RBI policy will affect access to microcredit by low income clients – 2011

READ MORE

M-CRIL’s Comments on the Malegam Committee Report

READ MORE

Promoting Financial Inclusion

READ MORE

Initial Public Offerings (IPOs): The Field’s Salvation or Downfall?

READ MORE